If you are looking for BCOE-143 IGNOU Solved Assignment solution for the subject Fundamentals of Financial Management, you have come to the right place. BCOE-143 solution on this page applies to 2021-22 session students studying in BCOMG courses of IGNOU.

BCOE-143 Solved Assignment Solution by Gyaniversity

Assignment Code: BCOE–143/TMA/2021-22

Course Code: BCOE-143

Assignment Name: Fundamentals of Financial Management

Year: 2021-2022

Verification Status: Verified by Professor

Maximum Marks: 100

Note: Attempt all the questions.

Section – A

Q1. Explain the meaning and objectives of financial management. (10)

Ans) Financial management entails the planning, arranging, directing, and managing of a company's financial activities, such as procurement and use of funds. It entails applying general management ideas to the company's financial resources.

Objectives

Financial management goals provide a framework for making the best decisions. The following are the two purposes of financial management:

Profit Maximization

Wealth Maximization

The objectives are means to reach to a goal of a business.

Profit Maximization

In broad terms, it means maximising the firm's profit. When we talk about this concept, it's a little hazy because it doesn't clearly state:

How much money do you make?

What is the absolute value of a share's earnings?

Is there a return on investment on the profits?

Is it better to measure profits before or after taxes?

Initially, this goal was the firm's primary goal, and there are numerous arguments in support of this. If a company embraces the profit maximisation philosophy, the returns will come later, which may not be healthy for the company's financial health. Profit maximisation is no longer a socially responsible decision on the side of the corporation. Let's look at some of the advantages and disadvantages of this strategy.

Pros

i) Resources utilized efficiently

ii) Measure of firms’ performance

iii) Serves the interest of the society

iv) Test of economic efficiency

Cons

i) Vague and ambiguous

ii) Ignores time pattern of profits

iii) Ignores risk and time value of money

iv) Ignores quality aspect of benefits

v) Unrealistic

vi) Ignores socially responsible behaviour

Wealth Maximization

This strategy aims to get beyond profit maximization's restrictions. The ultimate purpose of financial management is to achieve this. Profit maximisation, return on capital employed maximisation, growth in earnings per share or market value of a share or dividends, optimum degree of leverage, and cost of capital minimising are all operational concepts. In the modern approach to financial management, this is commonly acknowledged. This method, we may say, takes into account risk, appropriateness, and the temporal worth of money. This notion relates to the wealth of shareholders as measured by the market price of their stock. As a result, it entails maximising the firm's stock market price.

The net present worth of the firm can be calculated as follows:

Where A1, A2…… An= Stream of cash flows expected to occur from a course of action over a period of time;

W = Wealth

K = appropriate discount rate to measure risk and timing

C = initial outlay to acquire an asset

Therefore, we can say that wealth maximization concept is:

i) Unambiguous

ii) Measures risk

iii) Considers time value of money

iv) Socially responsible

This goal directs three financial management functions: investment, finance, and dividend. As a result, the primary goal is to maximise shareholder wealth, and profit maximisation might be regarded a subset of that goal. It's worth noting that if the time period is short and the risk is low, profit maximisation and wealth maximisation are nearly identical.

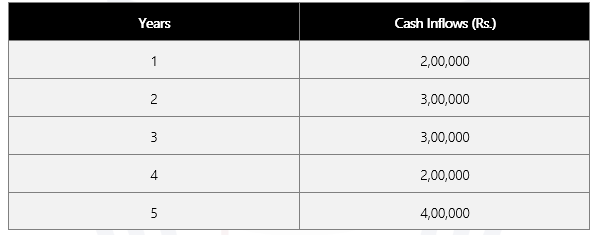

Q2. Calculate the NPV of a project which has an initial investment of Rs. 20,00,000/-, having a life of five years. The cost of capital is 8%. Should the company accept the project? Explain the reasons.

The cash inflows are as given below:

Ans)

Q3. Explain the different approaches for calculating cost of capital. (10)

Ans) The different approaches for calculating cost of capital are:

Because there is no coupon rate and the interest rate is not fixed as in preferred shares and debentures, determining the cost of capital is a difficult task. The rate of discount used to assess the present value of expected dividends is known as the cost of equity share capital.

Zero Growth Dividend

In this case, it is assumed that dividend will remain constant at:

Ke = D1/P0

Ke = Cost of equity share capital

D1 = Expected dividend at the end of year

P0= Current market price of the share( Net Proceeds)

g = growth rate

Constant Growth Rate in Dividends

It is assumed that dividends increase at a constant rate say ‘g‘ percent per annum.

Ke = D1/P0+ g

P0 = D0 (1+g)/Ke-g OR Ke = D1/P0 + g

P0 = D1/Ke-g

Varying Growth Rate in Dividend: Following is the equation considering varying growth rates in dividends:

Where G1 , G2, are the varying growth rates.

Earning-Price Approach

In this approach, the market price of the equity share depends upon the earnings. Earnings include both dividends and retained earnings whereas dividend approach does not include retained earnings.

Under this approach, cost of capital is calculated using following formula:

Ke= E0 / P0

Ke =Cost of Equity

E0 = Earnings Per Share

P0 = Net proceeds of an equity

Capital Asset Pricing Model (CAPM)

This procedure determines the return on any security based on the risk rating assigned to it. A security's expected return is directly proportional to the risk it represents. As a result, the risk-reward relationship is straight.

Risks associated with security investments can be divided into two categories:

Unsystematic Risk: It is diversifiable and is caused by company-specific elements like as management, employee dissatisfaction, strikes, and the firm's level of operational and financial debt. This portion of the total risk can be spread out.

Systematic Risk: It is non-diversifiable and results from macroeconomic factors such as changes in demand and supply, government policy, trade policy changes, inflation, purchasing power, and so on. The cost equity in CAPM is calculated using the risk-free rate, market return, and, which represents systematic risk.

Ke =Rf+ β (Rm–Rf)

Ke = cost of equity

Rf= risk –free return

β = coefficient of systematic risk

Rm= expected Market return

Realised Yield Approach

The problem in determining Ke using dividend price ratio and earning price ratio is estimating the rate of expected return. This strategy is predicated on the premise that actual profits from previous investments will be repeated in the future. Dividends paid and recorded in the past for a certain period should be taken into account when determining cost of equity. The most recent 5-10 years are used to compute the rate of return for an investor who bought a share at the start of the study period, held it until now, and sold it at the current price.

This is also the investor's realised yield. On the assumption that the investor earns what he expects to earn, this yield is designed to show the cost of equity shares. This strategy makes unreasonable assumptions, such as that the companies' risks remain constant, that shareholders demand the same rate of return, and that the shareholders' reinvestment rate is the same as the realised yield. This strategy is best suited towards companies with strong and consistent earnings.

Q4. From the following information, calculate the degree of financial leverage, degree of operating leverage and degree of combined leverage of a firm:

Ans)

Q5. Explain Baumol’s Model and Miller and Orr’s Model of cash management. (10)

Ans) Baumol’s Model and Miller and Orr’s Model of cash management:

The Baumol Model

Under specific conditions of certainty, William Baumol devised a cash model to estimate the optimal amount of transaction cash. The Economic Ordering Quantity (EOQ) model of inventory management was used to create this model. As we'll see later, EOQ refers to the number of units that need to be added to the business inventory in order to reduce the total cost of inventory maintenance and ordering.

The optimum cash level, according to the Baumol model, is the cash level with the lowest carrying and transaction costs.

The cost of storing cash, i.e. the interest foregone on marketable securities, is referred to as carrying costs (or holding costs).

The transaction costs are the costs associated with converting marketable securities into cash (such as clerical, brokerage, registration, and other fees).

The Miller-Orr Model

Merton Miller and Daniel Orr, two American economists, devised the model. The net cash flow is assumed to be totally stochastic in this scenario. According to the concept, cash withdrawals should be considered only when available funds fall below the money return threshold, which is established by the business's upper and lower cash balance restrictions. The lower limit is the minimum cash balance required to conduct a business, while the upper limit is the maximum cash level required.

The cash management normally sets the lower limit, which is determined by the company's creditworthiness, forecasted cash demands, and the acceptable risk of a cash flow gap. According to Miller and Orr, rather than determining the withdrawal amount, a corporation must determine the quantity of cash that must be kept on hand. They proposed that a corporation might have excess capital that could be put to better use by making investments to increase profits. This model is best suited to organisations with erratic cash flows.

Section – B

Q6. What is an operating cycle? Why is it important for the firm? (6)

Ans) The operating cycle is described as the time it takes for a corporation to purchase raw materials, make things, sell them, and earn cash from those sales. It's a key factor in determining how much working capital a company requires to run its day-to-day operations. To meet its business needs, a company with a very short operating cycle requires minimal working capital. If a company is a trading firm, its operational cycle is the time between when it spends money and when it receives money from its customers.

It consists of the following stages:

Purchasing raw material

Paying suppliers

Changing raw materials into work in progress/finished/final products

Selling finished/final products (Cash or credit)

Collecting cash from sale/receivables

The operating cycle is a metric for determining a company's operational efficiency. The operational cycle aids in calculating the amount of working capital a firm will require to properly operate and grow its business. A corporation with a very short operational cycle requires less cash to keep its activities running and is therefore favoured. A lengthier operational cycle, on the other hand, can cause cash flow issues.

Q7. What are the objectives of credit policy of a firm? (6)

Ans) Credit Policy relates to the amount and terms of credit that a company will extend to its consumers. Credit policy refers to a collection of guidelines and rules that govern trade credit supplied to clients. It regulates the amount of credit given to frequent customers on sales of goods and services in the course of business operations.

To facilitate huge volume sales, credit policies should be favourable. However, management should avoid adopting overly permissive credit practises, as this may result in the company incurring bad debts. Businesses should only extend credit to customers after determining their creditworthiness. A balanced credit policy is essential for good receivables management.

Credit Policy Objectives

Outlines Policies and Procedures: Effective credit policy communicates customers with various options in case they are not able to pay in full.

Provides Guidelines: Trade Policy helps outline the guidelines for legally collecting the money from slow or non-paying customers

Implements a Plan: An appropriate credit policy plan helps business in determining reasonable credit limits to be offered to the customers.

Outlines Steps: In order to eliminate bad debt, credit policy helps in outlining procedure and steps to collect dues from late paying customers.

Q8. What is economic order quantity? How is it calculated? (6)

Ans) The economic order quantity (EOQ) is a strategy for determining the optimal amount of an inventory order in order to reduce total inventory expenditures. It aids in the reduction of inventory keeping and ordering expenses over time. It indicates whether the current order quantity is reasonable or not.

According to this model, the formula for economic order quantity is as follows:

EOQ = √2AO / c

According to this model,

EOQ stands for Economic Quantity per order

A stands for total annual requirement for the item

O stands for ordering cost per order of that item

C stands for carrying cost per unit per annum

Example:

Calculate EOQ

Ordering cost - ₹ 10 per order

Annual quantity demand - 2000 units

Holding cost - ₹ 1 per unit per annum

Solution:

The formula for calculating EOQ is:

EOQ = √2AO / c

EOQ = √2 x 2000 x 10 / 1

EOQ = √40000

EOQ = 200 units

Q9. Discuss the advantages of lease financing. (6)

Ans) The advantages of lease financing are:

When an asset is purchased, there is always the danger of obsolescence, and the asset may become obsolete before its service life is completed. If the company leases the asset, the owner of the asset bears the risk of obsolescence. Firms must be aware, however, that the owner knows the true value of the equipment that is leased, allowing them to charge in accordance with the risk involved.

The company benefits from not having to pay for the asset right away and can use lease finance to acquire further assets.

If the asset was purchased with debt financing, the company would be subject to different terms and conditions set forth in the bond agreement. When compared to a loan, lease finance has significantly fewer constraints.

When a company takes out a loan to buy an asset, the debt includes both the asset and the loan. The obligation does not display as debt on the balance sheet in the event of lease financing. As a result, the firm's borrowing capability is strengthened.

Lease finance acts as a tax shelter for the company because it lowers its tax liability. When a firm leases an item, the entire lease payment is tax deductible, however if the company bought the equipment, it would be entitled to depreciation and interest deductions. The former strategy is far more advantageous to the business.

Q10. Explain the concept of return. (6)

Ans) The term "return" refers to receiving something in exchange for a financial investment. Because time is related with return, it is commonly referred to as rate of return. Return can be defined as the annual revenue gained as a result of a change in market price over a set period of time. The following formula is used to express this:

R = Dt + (Pt – Pt - 1) / Pt - 1

R = expected return

Dt = annual income/cash dividend at the end of time period

t = time period

Pt = share price at time period t (closing/ending share

We can understand the concept through an example.

Example

Suppose the price of a share X is `50 on April 1, 2020 (current year), annual dividend received is `.2 and the year-end price on March 31, 2021, is `55. What is the rate of return?

Solution:

D1 = 2

Pt= 55

Pt – 1 = 50

Substituting the values in the equation we get:

R = 2 + (55-50) / 50

R = 7 / 50

R = 0.14

R = 14%

This rate of return has two components viz.

Current yield

Capital gain/loss

Current Yield

Current Yield = annual income / opening price

In the above example, it will be

= 2 / 50

= 0.04

= 4%

Capital Gain/Loss

Capital gain/loss = closing price – opening price / opening price

If we substitute the values from the above example, we get :

Capital gain/loss = 55-50 / 50 = 5 / 50 = 1 / 10 = 0.10 = 10%

Therefore,

R = 14%

Current yield = 4%

Capital gain/loss = 10%

Returns can be realized or expected. Realized returns are the returns which

have already been earned by the firm and therefore, they become historic in

nature. Expected return is the anticipated returns which are to be earned in

future.

Section – C

Q11. Write short notes on the following: (5 x 4 = 20)

a) Valuation of convertible bonds

Ans) A convertible debenture/bond is a fixed-income debt asset that pays interest and can be exchanged into a pre-determined or fixed number of equity shares at any time. The debenture/bond can be changed into stock at any moment throughout the bond's life, usually at the bondholder's request. If an investor keeps the bond and does not convert it into stock, he will receive the face value when it matures. A convertible bond is a hybrid asset that provides investors with a flexible funding option for issuing corporations. It has bond characteristics such as a maturity date, coupon rate, face value, and payment of interest to investors over the life of the bond, as well as giving the investor the opportunity to acquire an equity share.

b) Internal Rate of Return method

Ans) The discount rate that makes the PV of cash withdrawals equal to the PV of cash inflows in an investment project is called the internal rate of return (IRR). The phrase 'internal rate of return' has three meanings. It is an investment's rate of growth, as well as the greatest rate of interest that an investor might pay on borrowed funds to finance the investment. The rate of discount (interest) that equates Net Present Value of cash inflows is the third interpretation.

The approval criteria for the IRR Method are as follows:

You must accept a project with an IRR greater than the cost of capital when making capital budgeting decisions. If you must pick between mutually exclusive projects, you must choose the project with the highest IRR among those with an IRR larger than the cost of capital.

c) Walter’s Model

Ans) Professor James E. Walter, a proponent of this approach, claims that a company's dividend policy has an impact on its market price. This model establishes the relationship between the firm's rate of return (r) and its cost of capital (k) in calculating the firm's dividend policy that maximises the firm's share market price.

The following stringent assumptions underpin Walter's assumption.

Internal Financing: All the investments of the firm are financed through retained earnings which imply that either, debt or new equity is not issued.

Constant Return and Cost of Capital: The firm’s rate of return (r) and its cost of capital (k) are constant throughout the life of the firm.

100 Percent Pay-out or Retention: The earnings of the firm are either paid as dividends in full or are retained in full to be reinvested immediately.

Retained Earnings are Only Source of Financing.

Constant Earning Per Share (EPS) and Dividend Per Share: The beginning earnings and dividends are not modified in this model; however the value of the EPS and Dividend may be changed to show the influence of dividend policy under different profitability assumptions. Any given EPS and Dividend value is supposed to remain constant during the course of the firm's life, which is assumed to be very lengthy and infinite.

d) Present Value

Ans) It is the amount of money received in future (FV) at a given time period (t) which is worth at present. The formula for calculating present value (PV) is as follows:

(2) PV = FV / (1 + rt)

Calculating Present Value (PV) based on Simple Interest

Let us understand this concept through an example.

Example:

Suppose the maturity value of a fixed deposit (FD) is ₹2,60,000. Calculate the initial amount of Fixed Deposit at which it has been purchased initially. The simple interest rate is 10% and the Fixed Deposit matures in 3 years.

Solution:

PV = FV / (1 + rt)

FV = 2,60,000

r = 10% = 0.1

t = 3

Substituting the figures in Equation 1

We get:

PV = 2,60,000 / [1 + (0.1 x 3)]

PV = 2,60,000 / 1.3

PV = Rs. 2,00,000

Therefore, PV is ₹2,00,000 for the Fixed Deposit.

100% Verified solved assignments from ₹ 40 written in our own words so that you get the best marks!

Don't have time to write your assignment neatly? Get it written by experts and get free home delivery

Get Guidebooks and Help books to pass your exams easily. Get home delivery or download instantly!

Download IGNOU's official study material combined into a single PDF file absolutely free!

Download latest Assignment Question Papers for free in PDF format at the click of a button!

Download Previous year Question Papers for reference and Exam Preparation for free!